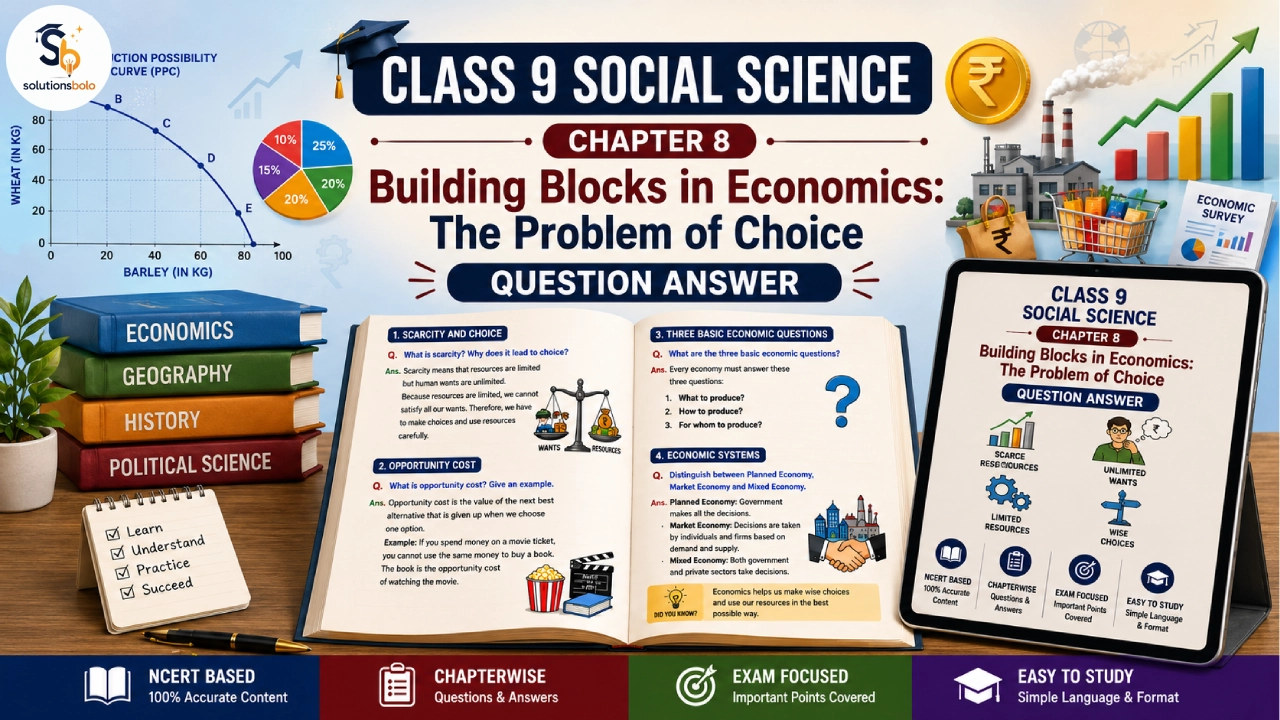

NCERT Class 9 Social Science Chapter 8 “Building Blocks in Economics: The Problem of Choice” introduces students to the basic concepts of economics and explains why individuals, enterprises and governments must make choices due to limited resources and unlimited wants. The chapter covers needs and wants, scarcity, opportunity cost, the Production Possibility Curve (PPC), the three basic economic questions, factors of production, economic systems (planned, market and mixed economies), data, surveys, the Economic Survey and the Union Budget. These NCERT Solutions provide clear explanations, key terms, intext answers, important questions, MCQs, assertion–reason questions, case-based questions, competency-based questions, long-answer questions, summaries and FAQs to help students build strong conceptual understanding and prepare confidently according to the latest CBSE syllabus (2026–27).

Table of Contents (Quick Links):

1. Chapter Introduction

2. Key Terms & Definitions

3. NCERT Intext Questions & Answers

4. NCERT Exercise Questions & Answers

5. Multiple Choice Questions (MCQs)

6. Assertion & Reason Questions

7. Hypothetical (HOTS) Questions

8. Competency-Based Questions

9. Common Mistakes Students Make & Exam Tips

10. Frequently Asked Questions (FAQs)

Chapter Introduction

Class 9 Social Science Chapter 8 Building Blocks in Economics: The Problem of Choice introduces the basic ideas of economics and explains why people, businesses and governments must make choices. Since human wants are unlimited but resources are limited, every decision involves a trade-off and an opportunity cost. The chapter also explains the three basic economic questions—what to produce, how to produce and for whom to produce—and compares planned, market and mixed economies. Understanding these concepts helps students relate economics to everyday life and make informed decisions about the efficient use of resources.

Key Terms and Definitions:

Building Blocks: The basic concepts that form the foundation of economics.

Economics: The study of how limited resources are used to satisfy unlimited needs and wants.

Market: A system where buyers and sellers interact to exchange goods and services.

Prices: The values at which goods and services are bought and sold.

Enterprise: An individual or organisation that produces goods or services.

Production: The process of creating goods and services using resources.

Needs: Essential things required for living.

Wants: Things people desire beyond their basic needs.

Choices: Decisions made because resources are limited.

Resources: Inputs used to produce goods and services.

Land: A natural resource used in the production of goods and services.

Labour: Human effort used in the production of goods and services.

Capital: Man-made resources used in the production of goods and services.

Factors of Production: Resources such as land, labour, capital and technology used to produce goods and services.

Opportunity Cost: The value of the next best alternative given up.

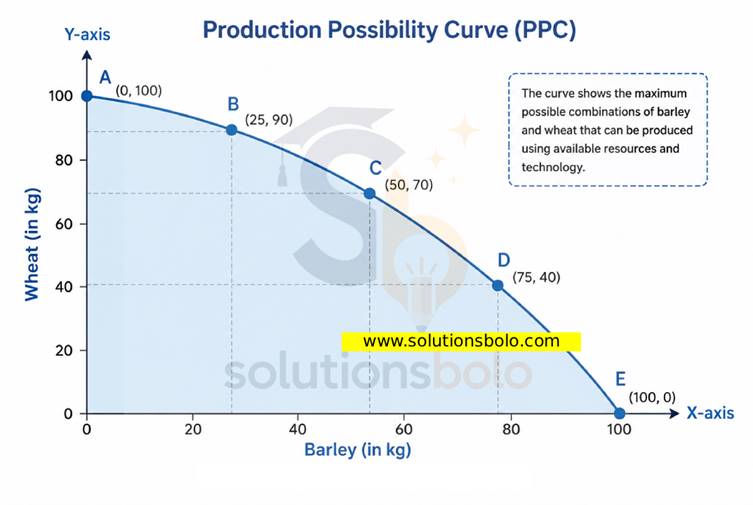

Production Possibility Curve (PPC): A curve showing the maximum possible combinations of two goods that can be produced using available resources efficiently.

Economy: A system for producing, distributing and consuming goods and services.

Economic Entities: Individuals or organisations involved in economic activities.

Data: Facts and information collected for analysis.

Management: The process of planning organising and using resources efficiently.

Limited Resources: Resources available in limited quantities.

Unlimited Wants: Human wants that can never be fully satisfied.

Optimising: Using resources in the best possible way.

Drive Investment: To encourage individuals or businesses to invest in productive activities.

Government Policies: Decisions made by the government to guide the economy.

Trade Influence: The effect of domestic or global trade on economic activities.

Infrastructure: Basic facilities that support economic activities.

Welfare Programs: Government schemes that improve people’s well-being.

Potential Outcomes: The possible results of a decision.

Surveys: Systematic collection of information for analysis.

Potential Risks: Possible future problems or uncertainties associated with a decision.

Policy Making: The process of developing government policies.

Research & Development (R&D): Activities to develop new knowledge, products or technologies.

Business Consulting: Providing expert advice to businesses.

Economic Survey: An annual report on the performance of the Indian economy.

Union Budget: The annual statement of the Government’s income and expenditure.

Ministry of Finance: The government ministry responsible for managing the country’s finances.

Blueprint: A detailed plan for future action.

Policymakers: People who make government policies.

Crucial Insights: Important information for better decision-making.

Scarcity: A situation where limited resources are not enough to satisfy unlimited wants.

Water-Intensive Crops: Crops that require large amounts of water.

Drought-Resistant Crops: Crops that can grow with very little water.

Trade-off: Giving up one option to gain another.

Income Levels: The amount of income earned by people or households.

Sustainability: Using resources wisely to meet present and future needs.

Labour-Intensive: Production that uses more labour than machines.

Capital-Intensive: Production that uses more machines than labour.

Automobile: A motor vehicle used for transportation.

Manufacturer: A person or company that makes goods.

Methods: Ways or processes of producing goods and services.

Technologies: The application of scientific knowledge, tools and techniques to improve production.

Planned Economy: An economy where the government makes major economic decisions.

Central Planning Authority: The government body that plans and controls the economy.

Planning Commission: The former government body responsible for India’s economic planning.

Government Ownership: Ownership of resources or enterprises by the government.

Private Ownership: Ownership of resources or enterprises by private individuals or firms.

Central Authority’s Targets: Production goals set by the central planning authority.

Permits and Licenses: Official approvals required for certain business activities.

Market Economy: An economy where markets mainly determine production and prices.

Intervention: Government action to influence economic activities.

Mixed Economy: An economy with both government and private sector participation.

Public Goods: Goods and services provided for the benefit of everyone.

Allocating Resources: Distributing resources among different uses.

Regulating Production: Controlling how goods and services are produced.

What to Produce: Deciding which goods and services should be produced and in what quantities.

How to Produce: Deciding which methods, resources and technology should be used to produce goods and services.

For Whom to Produce: Deciding who will receive the goods and services produced and how they will be distributed.

Public Policies: Government decisions made to achieve economic and social goals.

Global Trade: The exchange of goods and services between countries.

(Page – 183)

NCERT Intext Questions

1. What does economics deal with?

Answer:

Economics deals with the efficient use of limited resources to satisfy unlimited needs and wants by making informed choices and decisions.

Explanation:

Economics helps us to understand how individuals, enterprises and governments make decisions because resources are limited while human needs and wants are unlimited. It explains the importance of making choices, using resources efficiently, increasing production and improving living standards. Economics also helps in solving problems related to scarcity and supports better economic decision-making.

2. What are the key questions in economics?

Answer:

The key questions in economics are: What to produce, how to produce and for whom to produce using available resources efficiently.

Explanation:

Every economy has limited resources, so it must decide which goods and services should be produced, the best methods of production and who will receive them. These three questions help individuals, enterprises and governments allocate resources efficiently, satisfy people’s needs and promote economic development.

3. How do different economic systems address these questions?

Answer:

Different economic systems answer these questions through government control, market forces or a combination of both, depending on their economic structure.

Explanation:

In a planned economy, the government decides what, how and for whom to produce. In a market economy, these decisions are mainly made through market demand and prices. A mixed economy, like India, combines government intervention with private enterprise to achieve economic growth and public welfare.

(Page – 183)

4. Which type of crop should a farmer grow based on the condition of the soil, rainfall and market demand?

Answer:

A farmer should grow crops best suited to the soil, rainfall, available resources and market demand to maximise productivity and income.

Explanation:

Before choosing crops, farmers should carefully assess soil quality, water availability, weather conditions, production costs and market demand before choosing crops. Selecting suitable crops improves productivity, reduces the risk of crop failure, uses resources efficiently and helps farmers earn better income while supporting sustainable agricultural practices.

5. Should an enterprise employ more labour or capital in the production process?

Answer:

An enterprise should choose labour-intensive or capital-intensive production based on resource availability, production cost, technology and business requirements.

Explanation:

Generally, production depends on factors such as labour availability, wages, capital investment, technology, production scale and market demand. Enterprises compare costs and expected benefits to select the most efficient production method, ensuring higher productivity, better quality and long-term profitability.

6. Should the government spend more on building highways or hospitals?

Answer:

The government should allocate funds according to public needs, available resources and long-term national development rather than favouring only one sector.

Explanation:

Since government resources are limited, every spending decision involves a choice and an opportunity cost. It should analyse public needs, available funds and long-term benefits before allocating resources to sectors such as healthcare, education, transport or infrastructure for balanced development.

(Page – 184)

LET’S EXPLORE

7. List three things your parents bought this month. Can you classify them into needs or wants?

Answer:

My parents bought the following items this month: Rice – Need; Medicines – Need; New Bluetooth Speaker – Want. Needs are essential, while wants improve comfort or lifestyle.

Explanation:

Needs are goods and services required for a healthy and comfortable life, such as food, medicines and electricity. Wants are items people desire beyond basic needs, such as expensive gadgets, branded clothes or luxury products. The classification may differ depending on a family’s priorities, income and circumstances.

8. Do you think having too many wants may create problems? Why or why not?

Answer:

Yes, too many wants may create problems because resources are limited, making it impossible to satisfy every want at the same time.

Explanation:

Although human wants are unlimited, but income, time and resources are limited. Trying to satisfy every want may lead to unnecessary spending, poor financial decisions and overuse of resources. Economics teaches us to prioritise needs, make wise choices and use available resources efficiently.

(Page – 186)

LET’S EXPLORE

9. Ask your parents about how they make choices for everyday purchase. What is the opportunity cost of making a particular decision?

Answer:

My parents compare their needs, budget, quality and usefulness before making everyday purchases. For example, if they buy a school bag instead of a pair of sports shoes, the opportunity cost is the sports shoes they decided not to buy.

Explanation:

Families usually make purchasing decisions by considering their income, priorities, prices and future needs. Since money is limited, choosing one product often means giving up another. In economics, the value of the next best alternative that is sacrificed is called the opportunity cost. Understanding this concept helps families spend their money wisely and make better economic decisions.

Examples:

Buying groceries instead of a speaker.

Building a hospital instead of a stadium.

Saving money instead of buying a new mobile phone.

Growing wheat instead of sugarcane.

10. How do you decide to spend your time? Is time a scarce resource?

Answer:

I prioritise important activities such as studying and completing tasks. Yes, time is a scarce resource because it is limited and cannot be increased.

Explanation:

Every person has only 24 hours in a day, so time must be used wisely. Spending more time on one activity means giving up time for another. Therefore, managing time involves making choices and understanding opportunity cost, just like managing any other limited resource.

11. Should farmers produce water-intensive crops such as sugarcane and paddy or drought resistant crops such as millets and pulses?

Answer:

Farmers should choose crops according to water availability, soil conditions, rainfall, climate and market demand to ensure sustainable and profitable farming.

Explanation:

The choice of crops should depend on the availability of natural resources and local environmental conditions. In water-scarce regions, drought-resistant crops such as millets and pulses are more suitable, while water-intensive crops may be grown where sufficient water is available. Making the right choice improves productivity, conserves resources, reduces production risks and supports sustainable agriculture as well as long-term farmer income.

(Page – 189)

THINK ABOUT IT

12. Should the government allocate more funds to healthcare and education or to defence and space exploration? Why or why not?

Answer:

The government should allocate funds according to national priorities, public needs, available resources and long-term development, maintaining a balanced approach.

Explanation:

Government resources are limited, so every spending decision involves a choice and an opportunity cost. Before allocating funds, the government must consider public welfare, national security, economic growth and future development. A balanced allocation ensures that essential services such as healthcare and education, along with defence and technological advancement, receive appropriate support for the country’s overall progress.

(Page – 191)

LET’S EXPLORE

13. In your opinion, should the government completely stay out of enterprise decisions?

Answer:

No, the government should not completely stay out of enterprise decisions because appropriate regulation ensures fair competition, consumer protection and sustainable economic development.

Explanation:

Enterprises should have the freedom to make business decisions, but government intervention is necessary to protect consumers, prevent unfair practices, ensure environmental sustainability and promote public welfare. In a mixed economy like India, both the government and private enterprises work together to achieve balanced economic growth and efficient use of resources.

14. Can you think of an example where government action helped or harmed an industry or sector?

Answer:

Yes. Government investment in road infrastructure has helped transport, trade, tourism and manufacturing by improving connectivity and reducing transportation costs.

Explanation:

Government policies and investments can significantly influence different sectors of the economy. For example, building better roads and highways improves the movement of raw materials and finished goods, lowers transportation costs and increases business efficiency. As a result, industries expand, employment opportunities grow and economic development is promoted.

(Page – 193)

Exercise Question Answer:

1. Why do you think people’s wants keep changing over time? How does this affect production in an economy? Why cannot all our wants be satisfied?

Answer:

People’s wants keep changing due to changes in income, technology, lifestyles and preferences. This influences production as producers adjust to changing demand. However, all wants cannot be satisfied because resources such as land, labour, capital and time are limited.

Explanation:

Human wants are not fixed. As people’s income, education, technology, lifestyle and preferences change, they begin to demand new and better goods and services. Innovations and changing market trends also encourage consumers to replace old products with improved ones, leading to continuously changing wants.

Producers respond to changing consumer demand by:

(i) Producing new goods and services.

(ii) Increasing or reducing production based on market demand.

(iii) Adopting better technology and production methods.

(iv) Investing in new products and innovations.

Although human wants continue to increase, resources such as land, labour, capital, time and natural resources remain limited. Since every resource has alternative uses, individuals, enterprises and governments must make choices. Therefore, it is impossible to satisfy every want, making scarcity and opportunity cost unavoidable economic realities.

2. ‘Human wants are unlimited and keep changing’. How do you think this constant desire for more creates pressure on the environment? Can the fulfilment of wants and the extraction of resources be balanced?

Answer:

Unlimited and changing human wants increase the demand for natural resources, putting pressure on the environment. We should remember that resources are limited.

Explanation:

As people’s wants continue to increase, the demand for goods and services also rises. To meet this demand, industries require more raw materials, water, forests, minerals and energy. Excessive extraction of these resources can lead to deforestation, pollution, loss of biodiversity, resource depletion and climate-related environmental challenges.

Yes. A balance can be maintained between the fulfilment of wants and the responsible extraction of resources.

Fulfilment of Wants:

Human wants can be fulfilled through sustainable production, responsible consumption and efficient use of resources. Recycling and environment-friendly technologies help meet present needs while protecting nature.

Extraction of Resources:

Natural resources should be extracted responsibly and used efficiently. Conserving forests, water and minerals helps prevent resource depletion and ensures their availability for future generations.

3. Can you think of a resource in your region that is scarce but used wastefully? How could it be managed better?

Answer:

Fresh water is a scarce resource in many regions, yet it is often wasted through excessive use, leakage and poor management. It can be managed better through conservation, efficient use and sustainable water management practices.

Explanation:

In many regions, fresh water is one of the most valuable yet scarce natural resources. It is often wasted due to leaking pipelines, excessive irrigation, unnecessary household use and poor water management. As population and demand increase, the pressure on available freshwater resources also grows, making conservation essential.

Freshwater can be managed more effectively by conserving water, promoting rainwater harvesting, using efficient irrigation methods such as drip irrigation and repairing leaking pipelines to reduce water loss.

Efficient management of scarce resources helps reduce scarcity, supports sustainable development and ensures that resources remain available for future generations.

4. Which economic system—market, planned or mixed—do you think gives people the most freedom? Which economic system is best suited for promoting innovation? Why?

Answer:

A market economy generally gives people the most economic freedom because individuals and enterprises can make their own production and consumption decisions. However, a mixed economy is often better for promoting innovation because it combines private competition with government support and regulation.

Explanation:

1. Market Economy:

In a market economy, individuals and businesses have the freedom to decide what to produce, how to produce and what to buy or sell. Prices are mainly determined by demand and supply, with limited government intervention. This encourages competition, entrepreneurship and consumer choice.

Limitations:

• Income inequality may increase.

• Public welfare may receive less attention.

• Monopolies and unfair competition may develop.

2. Planned Economy:

In a planned economy, the government makes major economic decisions regarding production, prices and resource allocation. This system focuses on meeting national priorities and providing essential goods and services to everyone.

Limitations:

• Individuals and businesses have limited economic freedom.

• Innovation and competition may be discouraged.

• Decision-making can be slow and less flexible.

3. Mixed Economy:

A mixed economy combines the features of both market and planned economies. Individuals and private enterprises enjoy economic freedom, while the government regulates markets, provides public goods and protects public welfare.

Limitations:

• Excessive government regulation may affect business efficiency.

• Conflicts may arise between public and private interests.

• Balancing growth with social welfare can be challenging.

A mixed economy is often considered best for promoting innovation because it combines private competition with government support, encouraging new ideas, technological development and sustainable economic growth.

Such as: India’s Startup India initiative promotes entrepreneurship and innovation with support from both the government and the private sector.

5. Critically examine why pure economic systems rarely exist in reality. Assess the limitations of such systems and justify why a mixed economy is often considered a more practical and effective approach in real-world contexts.

Answer:

Pure economic systems rarely exist because no single system can meet all economic needs effectively. A mixed economy is considered more practical as it combines the efficiency of markets with government intervention to promote economic growth, public welfare and balanced development.

Explanation:

No country follows a completely planned economy or a completely market economy. Modern economies face diverse social, economic and environmental challenges that require both private enterprise and government participation. Therefore, most countries adopt a combination of both systems to achieve balanced and sustainable development.

Limitations of pure economic systems:

(a) A planned economy may reduce competition, limit consumer choice and slow innovation.

(b) A market economy may increase inequality, create monopolies and neglect public welfare.

(c) Neither system alone can effectively address all economic and social needs.

A mixed economy combines private enterprise with government participation. It promotes competition and innovation while ensuring public welfare, efficient resource allocation and balanced economic development.

6. A student has ₹100 and must choose between buying a notebook or saving the money for buying a tennis racket later. Which economic concept best explains this situation?

a. Demand

b. Opportunity cost

c. Production

d. Inflation

Correct Answer: (B) Opportunity Cost

Explanation:

The student has limited money and cannot choose both options at the same time. Buying the notebook means giving up the opportunity to save for the tennis racket, while saving the money means postponing the notebook purchase. The value of the next best alternative that is sacrificed is called opportunity cost. This concept helps people make better economic decisions when resources are limited.

7. How does understanding opportunity cost improve the quality of economic decision-making?

Answer:

Understanding opportunity cost helps people compare alternatives, evaluate benefits and sacrifices and choose the option that provides the greatest overall value from limited resources.

Explanation:

Every economic decision involves choosing one option and giving up another. Understanding opportunity cost encourages people to think beyond immediate benefits and consider what they are sacrificing before making a choice. This leads to more informed and rational decisions.

It helps people:

(i) Use limited money, time and resources efficiently.

(iii) Avoid unnecessary spending or wastage.

(iii) Select the option that provides the maximum long-term benefit.

8. Can effective economic decisions be made without reliable data? Support your answer with an example.

Answer:

No. Effective economic decisions require reliable data because accurate information helps individuals, businesses and governments make informed choices, allocate resources efficiently and reduce the risk of poor decisions.

Explanation:

Economic decisions should be based on facts rather than assumptions. Reliable data helps policymakers, businesses and individuals understand demand, production, prices, income and market conditions. This improves planning, reduces uncertainty and supports efficient use of resources.

Example: A company planning to produce umbrellas studies weather forecasts and customer demand before making production decisions. Reliable data helps it produce the right quantity and avoid unnecessary losses.

9. Analyse how a country’s present economic choices can shape its long-term future. Why is it important to consider future consequences while making economic decisions today?

Answer:

A country’s present economic choices influence its future growth, employment, infrastructure and living standards. Therefore, economic decisions should consider long-term consequences to ensure sustainable development and efficient use of limited resources.

Explanation:

Present Economic Choices and the Future:

Present economic choices influence a country’s future development. Investments in education, healthcare, infrastructure and technology improve productivity, create employment and support economic growth. Poor decisions, however, may slow development and create future challenges.

Considering Future Consequences:

Economic decisions should consider both present and future needs. Using limited resources wisely, avoiding wastage and protecting the environment help ensure sustainable development and improve the well-being of future generations.

10. Identify a news article from any newspaper of your choice about a product or commodity (such as vegetables, fruits, fuel or electronics) where producers or companies are deciding how much to produce or supply. Write 2–3 sentences explaining the example you found and why the production decision was made.

Answer:

A newspaper reported that automobile companies are increasing the production of Flex Fuel (E20-compatible) vehicles as India expands the use of ethanol-blended petrol. Manufacturers are adjusting production to meet changing government policies, rising consumer demand and the country’s goal of promoting cleaner and more sustainable fuels.

Explanation

Automobile manufacturers regularly adjust production according to market demand and government policies. As the use of ethanol-blended petrol (E20) expands in India, companies are increasing the production of Flex Fuel vehicles to meet future demand and support cleaner transportation.

This example mainly highlights:

Demand and supply

Economic decision-making

Production planning

Government policy and market influence

Efficient allocation of resources

This example illustrates how producers consider both present demand and future market conditions before deciding what and how much to produce.

Multiple Choice Questions (MCQs)

1. What is the main subject of economics?

(A) Studying different cultures

(B) Managing unlimited resources

(C) Using limited resources to satisfy unlimited needs and wants

(D) Producing only agricultural goods

Correct Option: (C) Using limited resources to satisfy unlimited needs and wants

Explanation:

Economics studies how individuals, enterprises and governments use limited resources to satisfy unlimited needs and wants. Since resources are scarce, economics helps people make informed choices and use available resources efficiently for maximum benefit.

2. Which of the following best explains the concept of opportunity cost?

(A) The total cost of production

(B) The value of the next best alternative given up

(C) The price paid for a product

(D) The income earned from production

Correct Option: (B) The value of the next best alternative given up

Explanation:

Opportunity cost is the value of the next best alternative that is sacrificed when a choice is made. Since resources are limited, choosing one option always means giving up another possible alternative.

3. Why do individuals and governments have to make choices?

(A) Resources are unlimited.

(B) Human wants are limited.

(C) Resources are limited but wants are unlimited.

(D) Production is always fixed.

Correct Option: (C) Resources are limited but wants are unlimited.

Explanation:

Choices become necessary because resources such as land, labour, money and time are limited, while human wants continue to increase. Economics helps decide how these scarce resources should be used efficiently and wisely.

4. Which of the following is one of the three basic economic questions?

(A) Where to produce?

(B) Who should own factories?

(C) What to produce?

(D) When to produce?

Correct Option: (C) What to produce?

Explanation:

Every economy must answer three important questions: what to produce, how to produce and for whom to produce. These questions help allocate limited resources efficiently and meet the needs of society.

5. In which economic system does the government make most major economic decisions?

(A) Market Economy

(B) Mixed Economy

(C) Planned Economy

(D) Open Economy

Correct Option: (C) Planned Economy

Explanation:

In a planned economy, the government decides what, how and for whom goods and services are produced. Major economic activities are controlled by a central planning authority instead of market forces.

6. Which economic system combines private enterprise with government participation?

(A) Planned Economy

(B) Traditional Economy

(C) Mixed Economy

(D) Command Economy

Correct Option: (C) Mixed Economy

Explanation:

A mixed economy combines the strengths of both market and planned economies. Private enterprises operate freely, while the government regulates markets, provides public goods and promotes public welfare and balanced development.

7. Which document reviews the performance of the Indian economy every year?

(A) Census Report

(B) Union Budget

(C) Economic Survey

(D) Five-Year Plan

Correct Option: (C) Economic Survey

Explanation:

The Economic Survey is an annual report that reviews the performance of the Indian economy. It provides important information and analysis that help policymakers prepare the Union Budget and frame economic policies.

8. A company replaces many workers with advanced machines to increase production. Which production method is being used?

(A) Labour-intensive production

(B) Capital-intensive production

(C) Traditional production

(D) Household production

Correct Option: (B) Capital-intensive production

Explanation:

Capital-intensive production uses more machines, equipment and technology than human labour. Enterprises choose this method to increase productivity, improve efficiency and reduce production time when appropriate technology is available.

9. Why is reliable economic data important?

(A) To increase prices only

(B) To reduce population growth

(C) To support better economic decisions and policy-making

(D) To eliminate all economic problems

Correct Option: (C) To support better economic decisions and policy-making

Explanation:

Reliable data helps governments, businesses and economists understand economic conditions, identify risks, forecast future outcomes and make informed decisions. It supports efficient resource allocation and better policy-making for economic development.

10. Why is sustainability important while making economic choices?

(A) It increases people’s wants.

(B) It avoids all production activities.

(C) It ensures resources are used wisely for present and future generations.

(D) It reduces the need for economic decisions.

Correct Option: (C) It ensures resources are used wisely for present and future generations.

Explanation:

Sustainability means using natural and economic resources responsibly so present needs are met without reducing the ability of future generations to meet their own needs. It promotes balanced and long-term economic development.

Assertion–Reason Questions

Directions: Choose the correct option.

(A) Both Assertion (A) and Reason (R) are true and Reason (R) is the correct explanation of Assertion (A).

(B) Both Assertion (A) and Reason (R) are true, but Reason (R) is not the correct explanation of Assertion (A).

(C) Assertion (A) is true, but Reason (R) is false.

(D) Assertion (A) is false, but Reason (R) is true.

1. Assertion (A): Every individual, enterprise and government has to make economic choices.

Reason (R): Resources are limited, while human needs and wants are unlimited.

(A) Both Assertion (A) and Reason (R) are true and Reason (R) is the correct explanation of Assertion (A).

(B) Both Assertion (A) and Reason (R) are true, but Reason (R) is not the correct explanation of Assertion (A).

(C) Assertion (A) is true, but Reason (R) is false.

(D) Assertion (A) is false, but Reason (R) is true.

Correct Option: (A)

Explanation:

Economic choices become necessary because resources such as land, labour, time and money are limited, whereas human needs and wants are unlimited. This scarcity makes decision-making an essential part of economics.

2. Assertion (A): Opportunity cost arises whenever a choice is made.

Reason (R): Choosing one alternative means giving up the next best alternative.

(A) Both Assertion (A) and Reason (R) are true and Reason (R) is the correct explanation of Assertion (A).

(B) Both Assertion (A) and Reason (R) are true, but Reason (R) is not the correct explanation of Assertion (A).

(C) Assertion (A) is true, but Reason (R) is false.

(D) Assertion (A) is false, but Reason (R) is true.

Correct Option: (A)

Explanation:

Opportunity cost is the value of the next best alternative that is sacrificed when one option is chosen. Since resources are limited, every economic choice involves giving up another valuable alternative.

3. Assertion (A): A mixed economy combines features of both planned and market economies.

Reason (R): A mixed economy promotes economic growth and public welfare.

(A) Both Assertion (A) and Reason (R) are true and Reason (R) is the correct explanation of Assertion (A).

(B) Both Assertion (A) and Reason (R) are true, but Reason (R) is not the correct explanation of Assertion (A).

(C) Assertion (A) is true, but Reason (R) is false.

(D) Assertion (A) is false, but Reason (R) is true.

Correct Option: (B)

Explanation:

Both statements are true. However, promoting economic growth and public welfare describes an outcome of a mixed economy, not why it combines features of planned and market economies. Therefore, Reason is not the correct explanation of Assertion.

Higher-Order Thinking Skills

1. Suppose the prices of raw materials and electricity suddenly increase. How do you think this will affect the production cost, selling price and quantity of goods produced by enterprises? Explain your reasoning.

| Think Like an Economist: |

When production costs increase, enterprises must decide how to respond. They may increase the selling price to recover higher costs. However, if higher prices reduce consumer demand, firms may produce fewer goods. Some enterprises may also adopt better technology, reduce wastage or use resources more efficiently to lower costs and remain competitive. This shows how production decisions depend on costs, demand and efficient resource allocation.

2. Suppose the prices of electronic goods fall sharply in the international market. How might this affect Indian producers, consumers and market competition? Give suitable reasons.

| Think Like an Economist: |

Lower international prices make imported electronic goods more affordable for consumers. This increases competition in the Indian market and encourages domestic producers to improve product quality, reduce production costs, adopt new technology or offer better services. Such competition benefits consumers by providing more choices and better value, while motivating producers to become more efficient and innovative.

3. Imagine that a severe drought reduces the availability of water in a farming region. How should farmers decide what crops to produce? Which economic concepts from this chapter would help them make the best decision?

| Think Like an Economist: |

During a drought, water becomes a scarce resource. Farmers should avoid water-intensive crops such as sugarcane and paddy and instead grow drought-resistant crops like millets and pulses. While making this decision, they should consider resource availability, market demand, expected income and the opportunity cost of each alternative. This reflects the economic concepts of scarcity, choice, opportunity cost and efficient resource allocation.

4. Suppose a garment factory installs advanced machines that can produce clothes much faster than before. How might this decision affect production, employment and opportunity cost? Do you think the decision is beneficial? Why?

| Think Like an Economist: |

Installing advanced machines increases production, improves product quality and reduces production costs over time. Although some manual jobs may decrease, new skilled jobs related to operating and maintaining machines may be created. The opportunity cost is the investment made in machines instead of other business activities. If the machines improve productivity and efficiency over the long term, the decision becomes economically beneficial.

5. Imagine the government has a limited budget and must choose between building a new hospital, a highway or a university. What factors should be considered before making the final decision? Which economic ideas from this chapter are involved?

| Think Like an Economist: |

When government resources are limited, every spending decision involves an opportunity cost. Before choosing a project, the government should study public needs, available funds, population, economic priorities and long-term benefits. Reliable data and surveys help in making informed decisions and allocating resources efficiently. This reflects the economic concepts of scarcity, choice, opportunity cost and efficient resource allocation.

Competency-Based Question:

Study the Production Possibility Curve (PPC) showing different combinations of barley and wheat production.

Suppose a new irrigation system and improved farming technology become available, allowing the farmer to produce more crops with the same amount of land and labour.

Answer the following:

(a) What is likely to happen to the Production Possibility Curve?

Answer: The Production Possibility Curve will shift outward because better technology increases production capacity.

(b) Which factor of production has improved in this situation?

Answer: Technology.

(c) How does improved technology help farmers make better economic choices?

Answer: It increases productivity, reduces wastage and enables more output from the same resources.

(d) Explain how technological improvement reduces the problem of scarcity but does not eliminate it completely.

Answer: Technology improves the efficient use of resources and increases production, allowing farmers to produce more goods. However, land, water, labour and capital remain limited, while human wants continue to grow. Therefore, scarcity is reduced but never completely removed and choices must still be made.

Common Mistakes Students Make in This Chapter (With Exam Tips)

1. Confusing needs with wants.

Exam Tip: Remember that needs are essential for living, while wants improve comfort or lifestyle.

2. Forgetting that resources are limited but wants are unlimited.

Exam Tip: This is the core concept of the chapter. Use it in descriptive answers whenever relevant.

3. Confusing opportunity cost with the price of a product.

Exam Tip: Opportunity cost is the next best alternative forgone, not the amount of money spent.

4. Memorising the three basic economic questions without understanding them.

Exam Tip: Learn what to produce, how to produce and for whom to produce with real-life examples.

5. Mixing up Planned Economy, Market Economy and Mixed Economy.

Exam Tip: Prepare a comparison table to remember the role of the government and private enterprises.

6. Confusing the Economic Survey with the Union Budget.

Exam Tip: The Economic Survey reviews the economy, while the Union Budget allocates government funds.

7. Ignoring the role of reliable data in decision-making.

Exam Tip: Remember that surveys and data help governments and businesses make informed economic decisions.

8. Thinking that higher profit is the only factor in production decisions.

Exam Tip: Also consider resource availability, technology, production costs and market demand.

9. Ignoring sustainability while making economic choices.

Exam Tip: Mention the efficient use of resources and future generations in long-answer questions.

10. Writing theory without relating it to daily life or current developments.

Exam Tip: Support your answers with simple and relevant examples such as water conservation, E20 fuel, electric vehicles (EVs) or rainwater harvesting.

Frequently Asked Questions (FAQs)

1. What is the main concept of Chapter 8 Building Blocks in Economics: The Problem of Choice?

Answer: The main concept of this chapter is that human needs and wants are unlimited, but resources are limited. Therefore, individuals, enterprises and governments must make choices and use available resources efficiently to achieve the maximum possible benefit.

2. Why is the problem of choice important in economics?

Answer: The problem of choice is important because resources such as money, time, land, labour and capital are limited, while human wants are unlimited. Economics helps people decide how to use these scarce resources wisely and efficiently.

3. What are the three basic questions every economy must answer?

Answer: Every economy must answer three basic questions:

(i) What to produce?

(ii) How to produce?

(iii) For whom to produce?

These questions help ensure the efficient allocation of limited resources.

4. What is opportunity cost in economics?

Answer: Opportunity cost is the value of the next best alternative that is given up when a person chooses one option over another. It is a key concept in economic decision-making because every choice involves a trade-off.

5. What is the difference between needs and wants?

Answer: Needs are essential for survival and daily living, such as food, clothing and shelter. Wants are things that improve comfort or lifestyle but are not essential for survival, such as luxury items and entertainment.

6. What is the difference between a Planned Economy, Market Economy and Mixed Economy?

Answer: In a Planned Economy, the government makes major economic decisions. In a Market Economy, decisions are made mainly through demand and supply. A Mixed Economy combines both systems, where the government and private enterprises work together.

7. Why is India called a mixed economy?

Answer: India is called a mixed economy because both the government and private enterprises participate in economic activities. The government provides public goods and welfare programmes, while private businesses produce goods and services and promote economic growth.

8. Why are data and surveys important in economics?

Answer: Data and surveys help governments and businesses understand economic conditions, identify problems, predict future outcomes and make informed decisions. They also support effective policymaking and the efficient allocation of resources.

9. What is the role of the Economic Survey and the Union Budget?

Answer: The Economic Survey reviews the performance of the Indian economy and provides important economic insights. The Union Budget presents the government’s plans for income, expenditure and resource allocation for the coming financial year.

10. How can students prepare Chapter 8 for exams?

Answer: Students should clearly understand the concepts of scarcity, needs, wants, choice, opportunity cost, production methods, economic systems, data, the Economic Survey and the Union Budget. Practising MCQs, case-based questions, assertion–reason questions and long-answer questions will improve conceptual understanding and exam performance.